Question 1. Explain market equilibrium.

Answer: Market equilibrium refers to the situation when market demand is equal to the market supply.

Question 2. What will happen if the price prevailing in the market is (i) Above the equilibrium price? (ii) Below the equilibrium price? Or How price and quantity are determined in the market when number of firms are fixed? Or How is equilibrium price of a commodity determined? (Use diagram). Or Explain why equilibrium price is determined at the level of output at which its demand is equal to its supply. Or How will equilibrium price be reached when there is excess demand/excess supply? Explain with diagram.Or With the help of a suitable diagram, explain the process of determination of equilibrium price of a commodity under perfectly competitive market. Or Market for a good is in equilibrium. Explain the chain of reactions in the market if the price is (i) higher than equilibrium price and (ii) lower than equilibrium price.

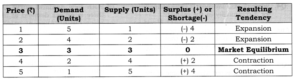

Answer: 1. Market equilibrium refers to that point which has come to be established under a given condition of demand and supply and has a tendency to stick to that level, i.e. where Demand = Supply. 2. If due to some disturbance we divert from our position the economic forces will work in such a manner that it could be driven back to its original position, i.e., where Demand = Supply. In short it is the position of rest. 3. It can be explained with the help of following schedule and diagram: (a) • In the below schedule market equilibrium is determined at Price 3 where Market demand is equal to Market Supply. • At price 1 and 2, there is excess demand, which leads to rise in price, resulting tendency is expansion in supply. • Similarly, at price 4 and 5, there is excess supply, which leads to fall in price, resulting tendency is Contraction in supply.

3. (b) • In the given diagram, price is measured on vertical axis, whereas quantity demanded and supply is measured on horizontal axis.

3. • Suppose that initially the price in the market is P1. At this price, the consumer demand P1B and the producer supply P1A, i.e. consumers want more than what the producer are willing to supply. There is excess demand equal to AB. So, price cannot stay on P1 as excess demand will create competition among the buyers and push the price up till we reach equilibrium. Due to rise in price from P1 to P, there is upward movement along the supply curve (expansion in supply) from A to E and upward movement along the demand curve (contraction in demand) from B to E. • Similarly, at price P2, the quantity demanded P2K is less than the quantity supplied P2L. There is excess supply, equal to KL, which will create competition among the sellers and lower the price. The price will keep falling as long as there is an excess supply. Due to fall in price from P2 to P there is downward movement along the supply curve (contraction in supply) from L to E and downward movement along the demand curve (expansion in demand) from K to E. • The situation of zero excess demand and zero excess supply defines market equilibrium (E). Alternatively, it is defined by the equality between quantity demanded and quantity supplied. The price P is called equilibrium price and quantity Q is called equilibrium quantity.

Question 3. When do we say there is excess demand for a commodity in the market?

Answer: When Market price is below the equilibrium price, then at that given price, demand is greater than supply, which leads to excess demand.

Question 4. When do you say there is excess supply for a commodity in the market?

Answer: When Market price is above the equilibrium price, then at that given price, demand is lesser than supply, which leads to excess supply.

Question 5. How are equilibrium price and quantity affected when income of the consumers 1. Increase? 2. Decrease?

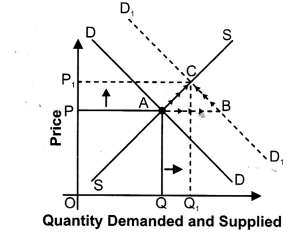

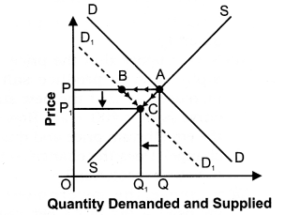

Answer: 1. Increase in Income: When income increases, demand curve will shift to rightward in case of Normal good as shown below: (a) As, we know normal goods are those whose quantity demanded varies positively with the change in income. As income of a consumer rises and goods consumed is normal goods equilibrium price and equilibrium quantity both rise. It can be shown with the help of the given figure.

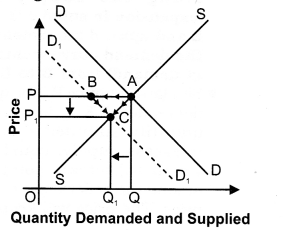

1. (b) In the given figure, price of normal goods is measured on vertical axis and quantity demanded and supplied are measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. (c) But as given in the examination problem when income of a consumer rises the demand of normal goods increases shifting the demand curve to the right from DD to D1D1. (d) With new demand curve DJDJ, there is excess demand at initial price OP because at price OP demand is PB and supply is PA; so there is excess demand of AB at price OP. (e) Due to this excess demand, competition among the consumer will raise the price. With the rise in price there is upward movement along the demand curve (contraction in demand) from B to C and similarly, there is upward movement along the supply curve (expansion in supply) from A to C . So, finally, equilibrium price rises from OP to OPi; and equilibrium quantity also rises from OQ to OQr Conclusion Due to increase in income of a buyer for normal goods, (a) Equilibrium price rises from OP to OP1. (b) Equilibrium quantity also rises from OQ to OQ1. 2. Decrease in income: When income decreases, demand curve will shift to leftward in case of Normal good as shown below: (a) As we know that normal goods are those whose quantity demanded varies positively with the change in income. As given in the examination problem if income of a consumer falls and goods consumed is normal goods, then both equilibrium price and the equilibrium quantity fall. It can be shown with the help of the given figure.

2. (b) In the given figure price of normal goods is measured on vertical axis and quantity demanded and supplied is measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. (c) But as given in the examination problem when income of a consumer falls the demand of normal goods also falls shifting the demand curve to the left from DD to D1D1. (d) With new demand curve D1D1 there is excess supply at initial price OP because at price OP demand is PB and supply is PA; so there is excess supply of AB at price OP. (e) Due to this excess supply competition among the producer will fall the price. Due to fall in price there is downward movement along the demand curve (Expansion in demand) from B to C and similarly, there is downward movement along the supply curve (Contraction in supply) from A to C. So, finally, the equilibrium price falls from OP to OP1 and equilibrium quantity also falls from OQ to OQ1 Conclusion Due to decrease in income of a buyer for normal goods, 1. Equilibrium price falls from OP to OP1. 2. Equilibrium quantity also falls from OQ to OQ1.

Question 6. Using supply and demand curves, show how an increase in the price of shoes affects the price of a pair of socks and the number of pairs of socks bought and sold. Or How will a rise in price of complementary affect the equilibrium price of given commodity? Explain the chain of effects.

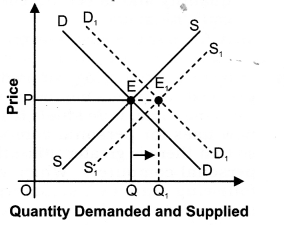

Answer: 1. As we know, shoes and pair of socks are complementary good to each other. As, price of complementary goods are inversely related with the demand of given commodity. So, rise in price of shoes (complementary good) decreases the demand for given commodity (pair of socks), and demand curve shifts leftward as shown in given figure:

2. In the given diagram, price is on vertical axis and quantity demanded and supplied is on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. 3. But due to rise in price of complementary good the demand curve of given commodity shifts leftward from DD to D1D1. 4. With new demand curve D1D1 there is excess supply at initial price OP because at price OP demand is PB and supply is PA; so, there is excess supply of AB at price OP. 5. Due to this excess supply, competition among the producer will fall the price. Due to fall in price, there is downward movement along the demand curve (Expansion in demand) from B to C and similarly there is downward movement along the supply curve (Contraction in supply) from A to C. So, finally, the equilibrium price falls from OP to OP1 and equilibrium quantity also falls from OQ to OQ1 So, due to rise in price of complementary goods, (a) Equilibrium price falls from OP to OP1 and (b) Equilibrium quantity also falls from OQ to OQ1 I.Very Short Answer Type Questions

Question 1. Define market equilibrium.

Answer: Market equilibrium refers to the situation when market demand is equal to the market supply.

Question 2. Give the meaning of equilibrium price.

Answer: The price at which equilibrium is reached is called equilibrium price.

Question 3. Give the meaning of equilibrium quantity.

Answer: The quantity bought and sold at the equilibrium price is called equilibrium quantity.

Question 4. What is equilibrium point?

Answer: Equilibrium point is the point of intersection of the demand curve and supply of commodity.

Question 5. When do you say there is excess demand for a commodity in the market?

Answer: When Market price is below the equilibrium price, then at that given price, demand is greater than supply that leads to excess demand.

Question 6. When do you say there is excess supply for a commodity in the market?

Answer: When market price is above the equilibrium price, then at that given price, demand is lesser than supply, that leads to excess supply.

Question 7. For a non-viable industry where does the supply curve lie relative to demand curve?

Answer: Supply curve lies above the demand curve.

Question 8. A severe drought results in a drastic fall in the output of wheat. Analyse how will it affect the market price of wheat?

Answer: Market price of wheat will increase (due to decrease in supply).

Question 9. What happens to equilibrium price of a commodity if there is ‘decrease’ in its demand and ‘increase’ in its supply?

Answer: Equilibrium price will fall.

Question 10. What happens to equilibrium price of a commodity if there is an ‘increase’ in its demand and ‘decrease’ in its supply?

Answer: Equilibrium price will increase. II. Short Answer Type Questions

Question 1. Under what condition increase in demand would not make any effect on equilibrium price?

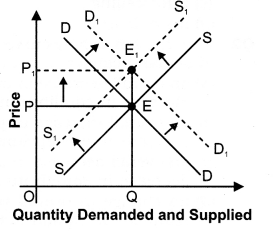

Answer: Case I: When supply also increase at the same rate as the demand increases In the given diagram price is measured on vertical axis and quantity demanded and supplied is measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. But when “demand and supply both increase at the same rate” then, 1. Equilibrium price remains – constant at OP; and 2. Equilibrium quantity rises from OQ to OQ1

Case II: When supply becomes perfectly elastic – In the given diagram price is measured on vertical axis and quantity demanded and supplied is measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. But when “supply becomes perfectly elastic and demand increases then, 1. Equilibrium price remains constant at OP; and 2. Equilibrium quantity rises from OQ to OQ1

Question 2. Under what condition increase in demand would not make any effect on equilibrium quantity?

Answer: Case I: When supply decreases at the same rate as the demand increase In the given diagram price is measured on vertical axis and quantity demanded and supplied is measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. But when, “demand increases and supply decreases but at the same rate”, then, 1. Equilibrium price rises from OP to OP1 and 2. Equilibrium quantity remains constant at OQ.

Case II: When supply becomes perfectly inelastic In the given diagram price is measured on vertical axis and quantity demanded and supplied is measured on horizontal axis. Initially, the equilibrium price is OP and equilibrium quantity is OQ. But when “supply becomes perfectly inelastic and demand increase” then, 1. Equilibrium price rises from OP to OP1 and 2. Equilibrium quantity remains constant at OQ.

Question 3. Give reasons for the following statements: 1. A decrease in supply will not result in a change in equilibrium quantity if the demand for a commodity is perfectly inelastic. 2. An decrease in supply will not result in a change in equilibrium price if the demand for a commodity is perfectly elastic.

Answer: 1. If the demand for a commodity is perfectly inelastic, i.e., if the demand curve is a vertical straight line, a decrease in supply curve will result only in a change in the equilibrium price, but no change in the equilibrium quantity. 2. If the demand for a commodity is perfectly elastic, i.e., if the demand curve is a horizontal straight line, a decrease in supply curve will result only in change equilibrium quantity, but no change in equilibrium price.

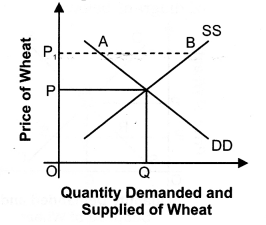

Question 4. Explain the effects of a ‘price ceiling’.Or Explain the effects of ‘maximum price ceiling’ on the market of a good. Use diagram.

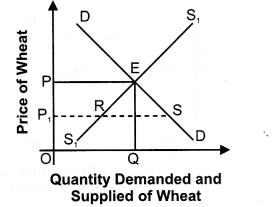

Answer: 1. When the government imposed upper limit on the price (maximum price) of a good or service which is lower than equilibrium price is called price ceiling. 2. Price ceiling is generally imposed on necessary items like wheat, rice, kerosene etc. 3. It can be explained with the help of diagram below:

3. (a) In the given diagram, DD is the market demand curve and SS is the market supply curve of Wheat. Suppose, equilibrium price OP is very high for many individuals and they are unable to afford at this price. (b) As wheat is necessary product, government has to intervene and impose price ceiling of Pi; which is below the equilibrium level. (c) Since this price is below equilibrium price, there is excess demand in the market. With shortages, sellers tend to hoard the product. It could also lead to black marketing.

Question 5. Explain the effects of a ‘price floor’. Or What are the effects of ‘price – floor’ (minimum price ceiling) on the market of a good? Use diagram.

Answer: 1. When the government imposed lower limit on the price (minimum price) that may be charged for a good or service which is higher than equilibrium price is called price floor. 2. Price Floor is generally imposed on agricultural price support programmes and the minimum wage legislation. 3. Since this price is above equilibrium price, there is excess supply in the market. Since there is surplus, sellers can attempt to sell their product at a price below the floor price.