Short Answer Type Questions

Q1. State the three fundamental steps in the accounting process.

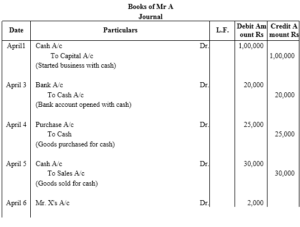

Answer :The fundamental steps in the accounting process are diagrammatically presented below.

Q2. Why is the evidence provided by source documents important to accounting?

Answer :The evidence provided by the source document is important in the following manners: 1. It provides evidence that a transaction has actually occurred. 2. It provides important and relevant information about date, amount, parties involved and other details of a particular transaction. 3. It acts as a proof in the court of law. 4. It helps in verifying transactions during the auditing process.

Q3. Should a transaction be first recorded in a journal or ledger? Why?

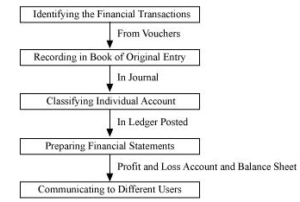

Answer :A transaction should be recorded first in a journal because journal provides complete details of a transaction in one entry. Further, a journal forms the basis for posting the transactions into their respective accounts into ledger. Transactions are recorded in journal in chronological order, i.e. in the order of occurrence with the help of source documents. Journal is also known as ‘book of original entry’, because with the help of source document, transactions are originally recorded in books. The process of recording the transactions in journal and then in ledger is presented in the below given flow chart.

Q4. Are debits or credits listed first in journal entries? Are debits or credits indented?

Answer :As per the rule of double entry system, there are two columns of ‘Amount’ in the journal format namely ‘Debit Amount’ and ‘Credit Amount’. The way of recording in a journal is quite different from normal recording. Journal entry is recorded in journal format in which the ‘Debit Amount’ column is listed before the ‘Credit Amount’ column. Credits are indented. Indentation is leaving a space before writing any word. Journal entry has its own jargon. While journalising, in the ‘Particulars’ column of journal format, debited account is written first and credited account is in the next line leaving some space, which is indentation.

Q5. Why are some accounting systems called double accounting systems?

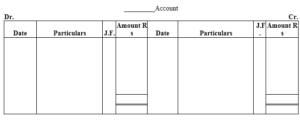

Answer :Some accounting systems are called double accounting systems because under this system there are two aspects of every transaction, i.e., every transaction has dual effect. Every transaction affects two accounts simultaneously, that is represented by debiting one account and crediting the other account. It is based on the fact that if there is receiver, there should be a giver. Q6. Give a specimen of an account.

Q7. Why are the rules of debit and credit same for both liability and capital?

Answer : Every business acquires funds from internal as well as from external sources. According to the business entity concept, the amount borrowed from the external sources together with the internal sources like, capital invested by the proprietor, is termed as liability to the business. Business entity concept treats business and business owner separately. Capital of the owner is treated as liability to the business because the business has to repay the amount of capital to the owner, in case of closure of the business. As liability incurred is credited, in the same way, fresh capital introduced and net profit increases the owner’s capital, and so, capital is credited. On the other hand, if liability is paid, it reduces liability, and so, it is debited. Similarly, drawings from capital and net loss reduce the capital, and so, capital is debited. Thus the rules of debit and credit are same for both liability and capital.

Q8. What is the purpose of posting J.F numbers that are entered in the journal at the time entries are posted to the accounts?

Answer :J.F. number is the number that is entered in the ledger at the time of posting entries into their respective accounts. It helps in determining whether all transactions are properly posted in their accounts. It is recorded at the time of posting and not at the time of recording the transactions. The purpose of entering J.F. number in the ledger is because of the below given benefits. 1. J.F. number helps in locating the entries of accounts in the journal book. In other words, J.F number helps to locate the position of the related journal entry and subsidiary book in the journal book. 2. J.F. number in accounts ensures that recording in the books of original entry has been posted or not.

Q9. What entry (debit or credit) would you make to: (a) increase revenue (b) decrease in expense, (c) record drawings (d) record the fresh capital introduced by the owner.

Answer : 1. Increase in revenue Increase in revenue is credited as it increases the capital. Capital has credit balance and if capital increases, then it is credited. 2. Decrease in expense Decrease in expense is credited as all expenses have debit balance. If expense decreases, then it is credited. 3. Record drawings Capital has credit balance; if the capital increases, then it is credited. If capital decreases, then it is debited. Drawings are debited as they decrease the capital. 4. Record of fresh capital introduced by the owner- credit Capital has credit balance, if capital increases, then it is credited. The introduction of fresh capital increases the balance of capital, and so, it is credited.

Q10. If a transaction has the effect of decreasing an asset, is the decrease recorded as a debit or as a credit? If the transaction has the effect of decreasing a liability, is the decrease recorded as a debit or as a credit?

Answer :If a transaction has a decreasing effect on an asset, then this decrease is recorded as credit. This is because, as all assets have debit balance and if assets decrease, then it is credited. For example, sale of furniture results in decrease in furniture (asset); so, the sale of furniture will be credited. If a transaction has a decreasing effect on a liability, then this decrease is recorded as debit. This is because all liabilities have credit balance. If the liability increases, then it is credited and if the liability decreases, then it is debited. For example, payment to the creditors results in a decrease in the creditors (liability); so, the creditors account will be debited.

Long Answer Type Questions:

Q1. Describe the events recorded in accounting systems and the importance of source documents in those systems?

Answer:It is beyond human capabilities to memorise each financial transaction and that is why, source documents have their own importance in accounting system. They are considered as an evidence of transactions and can be presented in the court of law. Transactions supported by evidence can be verified. Source documents also ensure that transactions recorded in the books are free from personal biases. A few events that are supported by source document are given below. 1. Sale of goods worth Rs 200 on credit, supported by sales invoice/bill 2. Purchase of goods worth Rs 500 on credit, supported by purchase invoice/bill 3. Cash sales worth Rs 1,000, supported by cash memo 4. Cash purchase of goods worth Rs 400, supported by cash memo 5. Goods worth Rs 100 returned by customer, supported by credit note 6. Return of goods purchased on credit worth Rs 200, supported by debit note 7. Payment worth Rs 1,200 through bank, supported by cheques 8. Deposits into bank worth Rs 500, supported by pay-in slips. Out of the above events, only those events that can be expressed in monetary terms, are recorded in the books of accounts. However, the non-monetary events are not recorded in accounts; for example, promotion of manger cannot be recorded but increment in salary can be recorded at the time when salary is paid or due. Source document in accounting is important because of the below given reasons. 1. It provides evidence that transaction has actually occurred. 2. It provides information about the date, amount and parties involved and other details of a particular transactions. 3. It acts as an evidence in the count of law. 4. It helps in verifying the transaction during the auditing process.

Q2. Describe how debits and credits are used to analyse transactions.

Answer : Debit originated from the Italian word debito, which in turn is derived from the Latin word debeo, which means ‘owed to proprietor’ and credit comes from the Italian word credito, which is derived from the Latin word credo, which means belief, i.e., ‘owed by proprietor’. According to the dual aspect concept, all the business transactions that are recorded in the books of accounts, have two aspects- debit and credit. The dual aspect can be better understood by the help of an example; bought goods worth Rs 500 on cash. This transaction affects two accounts with the same amount simultaneously. As goods are brought in exchange of cash, so the cash balances in the business reduce by Rs 500, i.e. why the cash account is credited. Simultaneously, the amount of goods increases by Rs 500, so purchases account will be debited. Debit and credit depend on the nature of accounts involved; such as assets, expenses, income, liabilities and capital. There are five types of Accounts. 1. Assets-These include all properties or legal rights owned by a firm for its operations, such as cash in hand, plant and machinery, bank, land, building, etc. All assets have debit balance. If assets increase, they are debited and if assets decrease, they are credited. For example, furniture purchased and payment made by cheque. The journal entry is: Furniture A/c Dr. To Bank A/c Here, furniture and bank balance, both are assets to the firm. As furniture is purchased, so furniture account will increase, and will be debited. On the other hand, payment of furniture is being made by cheque that reduces the bank balance of the business, so bank account will be credited. 2. Expense-It is made to run business smoothly and to carry day to day business activites. All expenses have debit balance. If an expense is incurred, it must be debited. For example, rent paid. The journal entry is: Rent A/c Dr. To Cash A/c Here, rent is an expense. All expenses have debit balance. Hence, rent is debited. On the other hand, as rent is paid in cash that reduces the cash balances, so cash account is credited. 3. Liability-Liability is an obligation of business. Increase in liability is credited and decrease in liability is debited. For example, loan taken from bank. The journal entry is: Bank A/c Dr. To Bank Loan A/c Here, loan from bank is a liability to the firm. As all liabilities have credit balance, so loan from bank has been credited because it increases the liabilities. 4. Income-Income means profit earned during an accounting period from any source. Income also means excess of revenue over its cost during an accounting period. Income has credit balance because it increases the balance of capital. For example, rent received from tenant. The journal entry is: Cash A/c Dr. To Rent A/c Here, rent is an income; hence, rent account has been credited and cash has been debited, as rent received increases the cash balances. 5. Capital-Capital is the amount invested by the proprietor in the business. Capital has credit balance. Increase in capital is credited and decrease in capital is debited For example, additional capital introduced by owner. The journal entry is: Cash A/c Dr. To Capital A/c As additional capital is introduced, so the amount of capital will increase, i.e. why, capital account is credited. On the other hand, as capital is introduced in form of cash, so the cash balances decrease, i.e. why, cash account is debited.

Q3. Describe how accounts are used to record information about the effects of transactions?

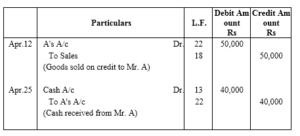

Answer : Every transaction is recorded in the original book of entry (journal) in order of their occurrence; however, if we want to know that how much we receive from our debtors or how much to pay to the creditors, it is not possible to determine at a single movement. Hence, we prepare accounts to know the position of business activities in the meantime. There are some steps to record transactions in accounts; it can be easily understood with the help of an example. Sold goods to Mr A worth Rs 50,000 on 12th April and received payment Rs 40,000 on 25th April. The following journal entries will be recorded:

Step 1- Locate the account in ledger, i.e., Mr A’s Account. Step 2- Enter the date of transaction in the date column of the debit side of Mr A’s Account. Step 3- In the ‘Particulars’ column of the debit side of Mr A’s Account, the name of corresponding account is to be written, i.e., ‘Sales’. Step 4- Enter the page number of the ledger in the Journal Folio (J.F.) column of Mr A’s Account. Step 5- Enter the amount in the ‘Amount’ column. Step 6- Same steps are to be followed to post entries in the credit side of Mr A’s Account. Step 7- After entering all the transactions for a particular period, balance the account by totalling both sides and write the difference in shorter side, as ‘Balance c/d’. Step 8- Total of account is to be written on either sides.

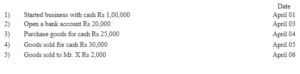

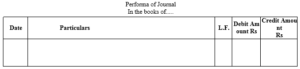

Q4 . What is a journal? Give a specimen of journal showing at least five entries.

Answer :Journal is derived from the French word Jour, means daily records. In this book, transactions are recorded in order of their occurrence, i.e., in chronological order from the source document. It is also termed as the book of original entry and each transaction is termed as journal entry.

Date- Date of transaction is recorded in the order of their occurrence. Particulars- Details of business transactions like, name of the parties involved and the name of related accounts, are recorded. L.F.- Page number of ledger account when entry is posted. Debit Amount- Amount of debit account is written. Credit Amount- Amount of credit account is written.