Concept of fair valuation in IFRS/Ind AS[/caption]

Concept of fair valuation in IFRS/Ind AS[/caption]

As you have read in my earlier articles, The whole world, including India, has moved into the concept of IFRS in the world while India has named them Ind AS. One of the significant aspects in them are the concepts of fair valuation. This means all companies which are following the IFRS or Ind AS standards for accounting, also needs to follow the fair value.

Simple words- what does it mean.

We have been following the concept of Historical based accounting. Example if I buy a flat in a Housing society say in 2003 for a value of 18 lacs, sitting in 2019, my books are still showing the value as 18 lacs less depreciation if any (if used for business purpose).

So Before IFRS/Ind AS, my Books would have showed

Gross value- 18,00,000

Less Depreciation- 6,00,000

Net value- 12,00,000

Now post IFRS/Ind AS implementation, I need to show them as per its fair value. What needs to be done is, get a property valuer, value it on current date. Suppose he says, the fair value is 2 crore then I need to pass an entry like this :

Asset - Debit - 1,82,00,000

Fair valuation Reserve- Credit 1,82,00,000

Impact of this entry:

a. Asset will increase to 2 cr ( 18 + 182) b. Fair valuation reserve will appear in the books at 1.82 cr

Benefits of this:a. Books will be reflective of the real scenario b. Assets will be represented by current values and so also the liabilities

New Changes due to fair valuation adherence which are now done are as under :

1. ICAI (institute of chartered accountants ) have come out with new valuation standards which needs to adhere while doing the valuations.

2. Ten standards have been issued for professional adherence

i) Preface to the Indian Valuation Standards ii) Framework for the Preparation of Valuation Report by the standards iii) Indian Valuation Standard 101 - Definitions iv) Indian Valuation Standard 102 - Valuation Bases v) Indian Valuation Standard 103 - Valuation Approaches and Methods vi) Indian Valuation Standard 201 - Scope of Work, Analyses and Evaluation vii) Indian Valuation Standard 202 - Reporting and Documentation viii) Indian Valuation Standard 301 - Business Valuation ix) Indian Valuation Standard 302 - Intangible Assets x) Indian Valuation Standard 303 - Financial Instruments3. Indian Valuation Standard 301 Business Valuation, issued by ICAI on 10th June 2018 shall be applied for the valuation reports issued on or after 1st July 2018.

4. These Indian Valuation Standards will be applicable for all valuation engagements on the mandatory basis under the Companies Act 2013 as per section 247 read with rule 18 of the Companies (Registered Valuers and Valuation) Rules, 2017.

5. In respect of Valuation engagements under other statutes like Income Tax, SEBI, FEMA etc, it will be on recommendatory basis for the members of the Institute.

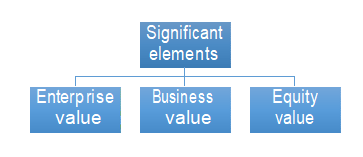

6. When valuing a business or business ownership interest, a valuer may express either an exact number or a range of values. There could be different benchmarks at which the estimate of value of an entity could be expressed by the Valuer as given below:

7. Business Value: Business value is the value of the business attributable to all its Shareholders.

7. Business Value: Business value is the value of the business attributable to all its Shareholders.

There are multiple methods in which a company can be valued. Some of these methods include:

a. Market Capitalization b. Times Revenue method c. Earnings Multiplier d. Discounted Cash Flow Method e. Book Value f. Liquidation Value

Business Value = (Enterprise Value- Market value of Debt)

8. Equity Value: Equity Value is the value of the business attributable to equity shareholders. Equity value uses the same calculation as enterprise value, but adds in the value of stock options, convertible securities, and other potential assets or liabilities for the company.

This method is commonly used to find out the value of equity shares during the sale/purchase of such shares

9. Generally, the following three main valuation approaches are adopted to perform the business valuation;

Market approach

A market approach is a valuation approach that uses prices and other relevant information generated by market transactions involving identical or comparable (i.e., similar) assets, liabilities or a group of assets and liabilities, such as a business. The following are the standard methodologies for the market approach:

(a) Market Price Method; (b) Comparable Companies Multiple Method; and (c) Comparable Transaction Multiple Method.

Income approach

Income approach is the valuation approach that converts maintainable or future amounts (e.g., cash flows or income and expenses) to a single current (i.e. discounted or capitalised) amount. The fair value measurement is determined based on the value indicated by current market expectations about those future amounts. The most commonly used income approach is Discounted Cash Flow method (DCF)

Cost approach

A cost approach is a valuation approach that reflects the amount that would be required currently to replace the service capacity of an asset (often referred to as current replacement cost). There are two methods here

(a) Replacement methods – Going concern basis (b) Liquidation methods - For not so going concern

Conclusion:

1. Standards are must to adhere.

2. Now the world will talk of fair values books and financial statements.

3. Three methods are significant.

4. Our Standards are based on international standards of valuation.